We are focusing on the Delta variant versus the strong earnings and macro data.

Push and Pull: Summary

- Growth is back, but for how long?: While earnings are shooting the lights out and growth stocks have outperformed, the overall market is tilting back toward a neutral/bearish sentiment and forward guidance is not as encouraging.

- The Delta variant is a stark reminder that the pandemic is not over: Until we have achieved global herd immunity, COVID-19 has still managed to find pockets of unvaccinated to allow for aggressive mutations.

- Follow the vaccinations: The money seems to be flowing across the pond as Europe catches up and surpasses the US in vaccination rates.

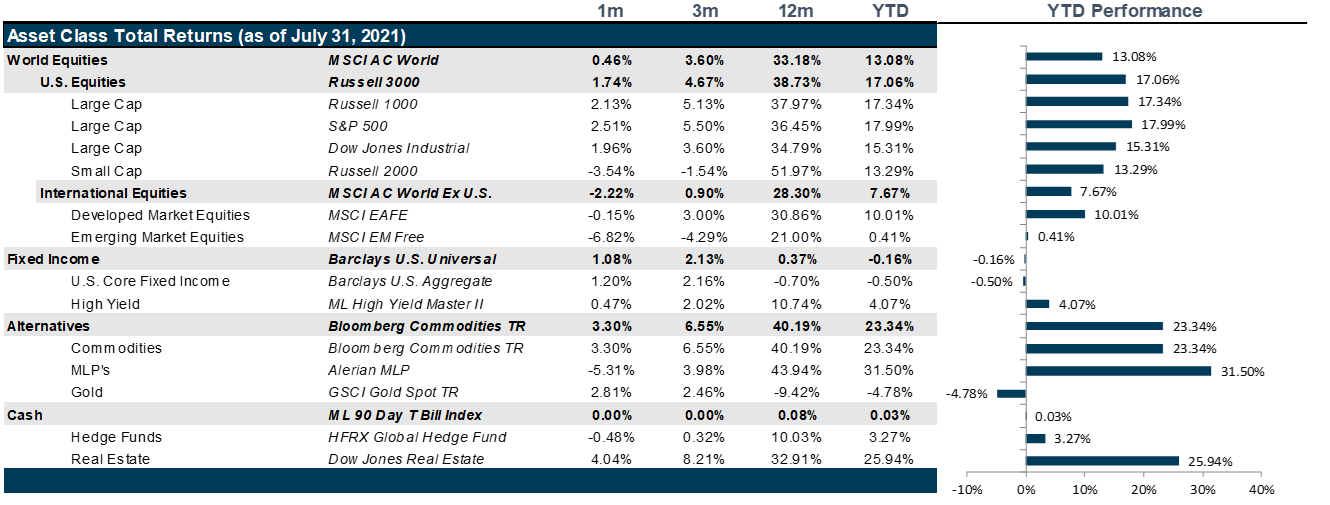

Market Review: Market See-Saw

Markets see-sawed in July as inflation concerns and the spread of the Delta variant worried investors, while earnings results painted a rosier picture.

At a glance, U.S. markets in July seemed to have continued the trend from the past months to touch new highs, however investor skittishness remained on full display as markets see-sawed from week-to-week, threatening to end the bull run at any moment. Inflation, which was the primary concern in the markets over the past quarter, took a backseat in July as the Delta variant of COVID-19 continued to spread at an alarming pace across the country, mainly targeting unvaccinated individuals. Weekly average of new cases increased by five times just in July. Further exacerbating sentiment, news filtered in that the Johnson & Johnson single shot vaccine may be less effective against the Delta variant. In addition, the labor market has not recovered at the pace expected by the Federal Reserve, and while officials have reiterated their stance on inflation remaining transitory, companies such as ConAgra, PepsiCo, and General Mills, which are directly involved in the purchases of raw goods, have raised the alarm on price surges. Towards the last two weeks of the month a slew of good earnings results posted by companies boosted markets, however those providing forward guidance painted a tepid picture for the second half of the year largely forecasting earnings growth to remain mostly flat.

In international markets, investor interest has grown for companies based within the eurozone, especially as the reopening-induced recovery trade starts to wind down in the U.S., and Europe begins to reopen with around 70% of the adult population receiving at least one dose of the COVID-19 vaccine. In addition, IHS Markit’s manufacturing PMI (purchasing manager’s index) tracking economic trends in the manufacturing sector, has continued to rise over the past three months providing support to the recovery trade storyline. Unlike their European counterparts, Japanese markets have not had a good month despite the commencement of the Summer Olympics, as stocks continue to remain pressured by mixed earnings results, the state emergency being extended in Tokyo, and other prefectures to contain the surging delta variant.

The MSCI Emerging Markets Index fell sharply in July as developing countries continue to lag their counterparts in vaccination rates and new variants continue to wreak further havoc on the population and economy. In addition, the high weighting of Chinese stocks in indexes tracking emerging markets has had a negative impact over the past month. As the Chinese government continues to crackdown on technology companies, with the latest target being the ride-hailing giant Didi Global Inc., that was placed under scrutiny by the government over cybersecurity concerns just days after its listing on the New York Stock Exchange. In addition, the Chinese government has also demanded that the $120 billion private-tutoring sector to turn non-profit, resulting in stocks such as TAL Education Group plummeting by 70.7% in a single day.

Inflation concerns and a loose monetary policy centered around a long-term average inflation rate of 2% rather than a fixed threshold of 2% has continued to plague bond investors over the past three months. Weekly jobless claims have continued to stagnate between 360,000 – 400,000 and the labor markets seem to have hit a wall in recovery after an accelerating start, causing investors to question the Federal Reserve’s dovish stance. Between July 1st and July 19th, ten-year yields dropped by 29 bps to a low of 1.19%, a number not seen since February, as investor anxiousness over the potential growth impact of the Delta variant rushed into treasuries. While the bond market clawed back some gains in yields as positive earnings results caused some investors to jump back on the equity bandwagon, slowing economic growth data out of China reinvigorated the worry that the U.S. recovery could easily turn into the kind of stagnation currently occurring in China.

Crude oil prices dropped as low as 9.6% before recovering this past month as the OPEC+ reached an agreement to boost supply, and gold prices surged to a high of $1829 over inflationary concerns. An uneven global economic recovery coupled with wild weather fluctuations throughout the world has thrown the demand-supply balance into disarray. Prices of wheat, coffee, oats, and tea increased by an average of 15% over the past month as crop outlooks deteriorated in response to worsening weather conditions. In the cryptocurrency universe, stablecoins have become the latest instruments to be targeted by financial regulators especially as they mimic the current monetary system but exist out of the purview of the central banks. In addition, they also pose a monetary risk in the sense that pegging the value of the stablecoin to a fiat currency such as the U.S dollar allows for double lending on the same asset.

Going Forward: Push and Pull

Expectations matter. When expectations were dismal, any positive news seemed like a miracle. But now that expectations are high, the hurdle for a positive surprise is now difficult to achieve. For the first time in a year the Citibank Economic Surprises Index for the U.S. turned negative while we had our first broad survey downward revision for U.S. growth, according to the Bloomberg survey of economists. Further supporting this state of apprehension, U.S. yield curves bear-flattened with the long end falling as concerns around inflation went right out the window and concerns about the Delta variant drove the ten-year to 1.22%. Meanwhile, we have hit a peak for earnings growth, economic growth expectations, and labor market recovery in the U.S. So, is the party over?

The Continuing COVID Saga

As the vaccination push brought a dramatic drop in new caseloads, hospitalization rates, and death rates, it seemed that life in the United States might get back to normal. Businesses reopened, mask mandates were dropped and the country breathed a collective sigh of relief. This was quickly followed by a collective sigh of exasperation as the Delta variant emerged in unvaccinated pockets around the world spread into our own backyard among unvaccinated individuals. The new Delta variant, considered dramatically more transmissible by as much as 40-60% as the original Wuhan strain with viral loads as much as 1,000 times higher, has swept the globe. This was then followed by a gasp of concern as a small number of breakthrough infections hit vaccinated individual and talk of booster shots began to circulate. And, just like that, mask mandates were re-imposed and a general air of concern now permeates consumption decisions. As the summer re-opening boom begins to stall in the U.S., Europe has hit a gallop in terms of both vaccination rates and vaccination passes to support the reopening even in the midst of the Delta variant and other variants of concern. In China, the reopening has now evolved to stagnation while Japan, who should have been experiencing the fruits of the Olympics, are instead mired in a state of emergency. Though European earnings are largely peaking this quarter as well, pricing for European equities is significantly more attractive, having fallen below long-term averages. With markets shifting to more stable or less expensive assets, Europe could benefit.

Fiscal Spending

In the U.S., the big offset to the recent market wobbles is the Infrastructure Investment and Jobs Act, a $1 trillion infrastructure bill for roads and bridges, broadband internet, public transit, and electric utilities expected to generate two million jobs per year over the next decade. This is expected to be followed by a companion $3.5 trillion spending bill that Democrats hope to pass through budget reconciliation that will include spending earmarked for climate change, childcare, housing, job training and education. Given the current state of the US government balance sheet it is easy to focus on the cost side of this equation, yet multiple studies suggest that positive impacts of infrastructure investment have large multiplier effects beyond the jobs created that would offset the impacts of deficit financing. However, offsetting is not surpassing, which is to say that while it seems like a positive thing to do, the passage of the infrastructure bill will be unlikely to significantly change the already positive outlook priced into U.S. equities. But not all equity analysts are good at math. So, it still could.

Emerging Markets Vulnerability

What is very clear is that many emerging market countries remain significantly vulnerable to COVID and companies that have outsourced significant portions of their supply chains to these countries in return for lower labor costs have discovered the price of dependability and stability. As commodity prices reflect the most basic shortages of labor, prices of intermediate goods are also creating inflation in the U.S. that could become permanent by virtue of onshoring. The great reversal in manufacturing may well be a boon to U.S. workers, cities, and states, it will also represent a jump in costs that will not be transitory, as the Fed suggests. The only scenario where the costs remain low is if onshoring occurs through automation, in which case expect a rise of the robot tax discussion. Either way, we see pressure on margins coming down the pike.

Net View

We remain neutral in U.S. equities on size and style. We also remain underweight Emerging Markets relative to US and add an overweight to Europe relative to Japan.