We explore the challenges of market peaks and the psychology of downward revisions.

Peak Markets: Summary

- Equity markets continue to climb the wall of worry: FOMO is keeping investors in growth stocks but the delta variant and the peaking of market expectations and the end of easy comps are creating market volatility making for challenging markets.

- Supply chain disruptions and labor market shortages continue to test market patience in the transitory inflation concept: ten-year bond yields are being driven primarily by delta variant risks sending them well above what the long end can eke out with rangebound breakeven inflation and minor downward revisions to very strong GDP growth expectations.

- International markets remain mixed with vaccination rates the most important metric: Europe’s 70%+ vaccination rate continues to shine through with GDP growth revisions and expectations still on the upswing.

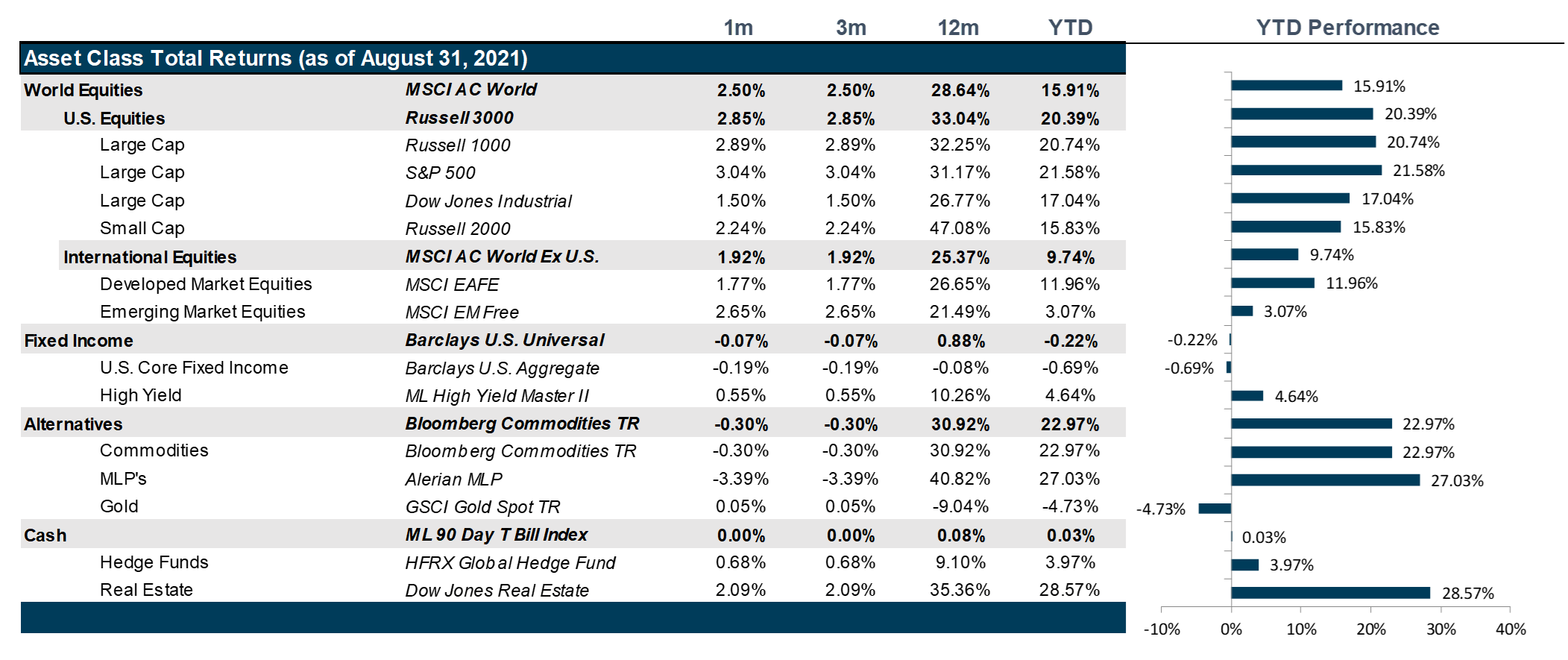

Market Review: Interesting Times

Key influencing events over the course of August include the Senate’s passage of the infrastructure bill in the first week, the spread of the delta variant in the second week, the dramatic fall of the Afghan government to the Taliban following the departure of the U.S. military in the third week, and the Federal Reserve’s Jackson Hole Symposium in the final week.

U.S equities hit new record highs in August as loose monetary policy and record low interest rates have made investors loath to shift away from equities. President Biden’s $1.2 trillion infrastructure bill passed the Senate towards the end of the first week, boosting equities, particularly in the utilities sector. However, the increase in the delta variant caseload combined with lackluster progress on vaccinations ushered in a bout of volatility. Adding to the volatility, the fall of Afghanistan’s government and subsequent takeover by the Taliban led to a major selloff in broad equities and rotation towards the growth sectors of technology and communication services. Weekly jobless claims have fallen to the levels of 350K, and nonfarm payroll numbers continue to improve from month-to-month, however the recovery in employment seems to fall short of the Federal Reserve’s expectations. Minutes from the latest FOMC meeting and news from the Jackson Hole Symposium reverberates the same content: the Federal Reserve considers the current inflation numbers to be transitory and may start to taper on the monthly $120 billion bond purchases by the end of the current year, but a rate hike is not expected any time soon. Investors continue to remain concerned as Quarter-over-quarter GDP growth over the second quarter came in below expectations. Growth is primarily driven by government spending, investments, and post-vaccination consumption demand. But, net exports continue to fall as other countries lag in vaccinations. And, though, personal spending is reverting to normal and personal income is rising, inflation threatens to run hot and the biggest fear on investor minds is the Federal Reserve being unable to commandeer the mammoth vessel that is the U.S economy as we float further into unchartered waters.

In international markets, Europe continues to benefit from investor interest and rose for the seventh consecutive month, suffering a blip in the middle of the month when the U.S withdrew from Afghanistan and the Taliban toppled the previous government. While the spread of the delta variant continues to remain a concern, many governments plan on providing booster shots, buoying investor sentiment. While Europe has largely stemmed the rise in new cases by vaccinating roughly 70% of their population, Japan continues to be plagued by a slow vaccine rollout as well as vaccine recalls due to contamination, resulting in extended lockdowns and a slower than expected recovery.

Emerging market indexes continue to underperform their developed counterparts with China as the primary laggard. China was one of the first countries to emerge from lockdown. The government has taken advantage of the discrepancy in recovery timelines between nations to increase regulatory oversight in key sectors such as finance, technology and education, without causing a seismic rotation out of Chinese equity markets. Record low rates around the world, a surge of individual investors as well as thematic ETF’s and ballooning government balance sheets in the west have left investors stuck between a rock and a hard place, in search of yield and stability and keeping them invested in China.

The yield curve steepened in August, reacting to falling unemployment claims, and improving numbers of nonfarm payrolls. Breakeven inflation numbers have also been exhibiting low volatility, however there are lingering signs of investors losing confidence in the Federal Reserve. Future monetary policy appears dependent on yet another raising of the debt ceiling and Jerome Powell being reinstated as Fed Chairman; a more dovish Fed Chairperson could spook markets heavily. In addition, the notion of transitory inflation being pushed by Fed officials largely rests on dampening the disruptions to global supply chains due to mutating versions of the coronavirus and labor shortages. Should either of the two remain persistent in the foreseeable future, central banks will be forced to scale up the pace of tightening their monetary policies, resulting in investor attention shifting towards the underlying credit qualities of each security, and a repeat of the European debt crisis but on a much larger scale.

Oil prices have continued to remain stable over the past month as the OPEC+ continues to raise production levels slowly. There have been fluctuations in WTI crude oil prices owing to the extreme weather conditions as well as reported drop in inventory levels. Extreme weather conditions have also pushed up food prices globally as a supply shortage for commodities such as wheat has driven exporters to hold onto stock. Precious metals such as gold and silver, have been focused on employment data, surging in price at the slightest sign of growth slowdown, however they now also have to compete with cryptocurrencies which are fast carving a niche for themselves in investor portfolios as an inflation hedge.

Going Forward: Peak Markets

The greatest danger in any market is the point at which strong performance begins to underperform even stronger expectations. What tends to follow is a game of catch up with downward revisions and moderating and less and less positive earnings. And, though in the case of the U.S., we are talking about GDP moderating from 6.3% to 4.3%, still well above long term trend growth and earnings slowing from 92% Quarter-over-quarter comps to an average of 10% Quarter-over-quarter comps over the course of the next four quarters. These are strong numbers, but the psychology combined with the frothiness in valuations and the potential for tapering or a rate hike certainly make the markets less appealing than before. The big question in our minds concerns the level of employment and activity we can expect once we get back to “normal” whenever that is. Will personal incomes, consumption and business investment settle back into previously established trends or will they be faster or slower. What we know is that much has changed in the past year and a half and some of the changes will fundamentally change the outlook for certain companies, sectors, and market segments. The trick is to anticipate the winners and losers.

The Cloud

As the vaccination push brought a dramatic drop in new caseloads, hospitalization rates, and death rates, it seemed Many of the trends that were in place prior to the pandemic including the move into cloud computing and storage and business continuity were already in place prior to the pandemic and in many ways, facilitated the quick adoption of remote work by many companies. Those segments of the technology sector remain attractive even despite some pricy valuations as the movement continues to gain strength. However, this will also facilitate professional services under the Industrials umbrella which run the gamut from outsourced services to consulting services that can be more efficiently delivered through virtual means.

Infrastructure

In the U.S., the big offset to the recent market wobbles is the Infrastructure Investment and Jobs Act, a $1 trillion In addition, Infrastructure spending remains a highly anticipated economic stimulus measure that will certainly benefit planes, trains and automobiles, but not necessarily electric automobiles, which didn’t get quite the allotment Democrats originally pushed for. However, there will be some significant investment into Amtrack and airport upgrades which will benefit industrials, materials and commodities fairly broadly. The investment of internet infrastructure into poorly serviced areas will be an enormous boon to internet providers and all of the communications services that rely on that ethernet highway. However, no one could agree on how to fund this massive spending with Democrats baulking at a gas tax and Republicans balking at a rise in corporate taxes. So, they are going after cryptocurrency gains instead, which could be a big loser in 2022 as the tax reality bites the average investor.

Vaccinations

What is very clear is that many emerging market countries remain significantly vulnerable to COVID and companies Vaccine hesitancy in wealthy countries remains a greater impediment to ending the pandemic than the lack of vaccine availability in poor countries, though both present real problems. Europe is leading the charge at this point, having crossed the 70% threshold for vaccinated adults just ahead of the U.S. in late July. Because Europe had not experienced the run up in expectations, the upward revisions occurring now have a greater potential to be sustainable as the bloc reopens. However, the lack of vaccine availability in poorer countries remains a significant concern as supply chain disruptions are driving a massive re-shoring of manufacturing in wealthy countries like the U.S. and Europe. This could leave some Emerging Market countries far worse off after the pandemic subsides.

Net View

We remain neutral in U.S. equities on size and style. We also remain underweight Emerging Markets relative to U.S. and add an overweight to Europe relative to Japan.