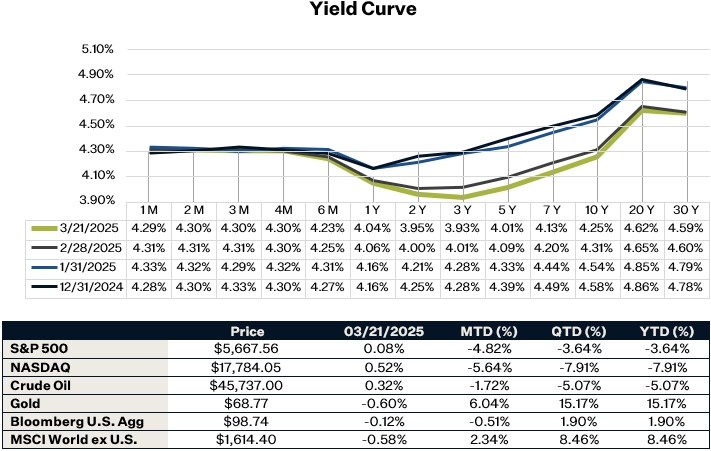

Market Update

The S&P 500 was flat last week as investors digested the Fed’s decision on Wednesday seeing that Jerome Powell brought back “transitory inflation” pertaining to the tariffs providing some fear relief. On Friday, U.S. stocks ended the day mostly flat, recovering from earlier losses after comments from President Trump eased concerns about the potential impact of April 2nd tariffs saying there will be some “flexibility”. Despite both “transitory inflation” and “flexibility” regarding tariffs, the market and the U.S. economy remain in this stage of uncertainty as there is no clear end game regarding trade policy, economic growth and monetary policy. Looking ahead, key data releases this week include S&P Global’s flash PMI, offering insight into business sentiment across the manufacturing and services sectors, as well as the latest reading on the Consumer Confidence Index.

FOMC March Meeting

As expected, the Federal Reserve kept rates unchanged last week at 4.25% - 4.5%. The market was anxiously waiting for an update in the Fed’s Summary of Economic Projections, which showed several notable changes from their December forecasts. For one, the committee significantly lowered their GDP growth forecast for this year – from 2.1% in December to 1.7% this month. Additionally, they raised their inflation forecasts. The committee is now expecting headline PCE inflation to be 2.7% at the end of the year compared to 2.5% in December. They now see no further progress in core PCE inflation this year but instead see an increase in Core PCE levels, expecting Core to be 2.8% at the end of year. Given that the Fed is now expecting lower growth but higher inflation, they kept the predicted number of rate cuts to 2 this year.

During the press conference, Powell said “uncertainty is unusually elevated”, making the economic growth outlook tough to predict. When it comes to tariffs and inflation, Powell mentioned that some of the recent pickup in goods inflation is likely coming from tariff expectations, however it is very difficult to determine exactly how much is linked to tariffs. The current economic environment is making the Fed’s job increasingly difficult – the possibility of stubborn inflation supports a more hawkish stand while a weaker growth backdrop would suggest potential need to cut rates more rapidly. The market is still expecting a rate cut in June, with another cut expected in September or October.

Existing Home Sales

Existing home sales rose 4.2% in February, against expectations for a decline (see "USA: Existing Home Sales Above Expectations"). And the median sales price of all existing homes was up 3.8% yoy, highlighting the supply- constrained nature of the US housing market. Even though existing homes sales are still tracking about 20% below pre-pandemic levels, the homes that are selling, are selling for a high price, suggesting the demand to move is there.

Sources:

https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20250319.pdf

https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

https://www.nar.realtor/research-and-statistics/housing-statistics/existing-home-sales