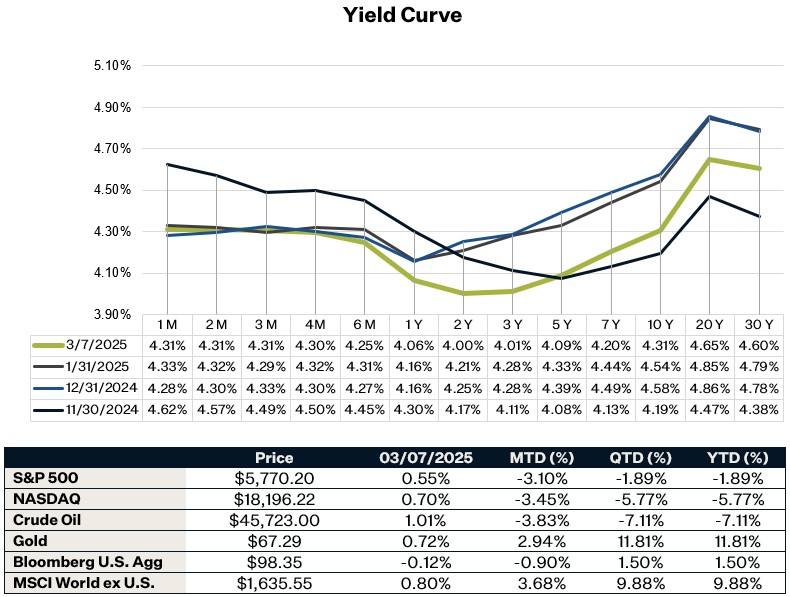

Market Update

Concerns around economic growth caused by the uncertainty around tariffs continued to weigh on markets last week, with the S&P 500 falling 3.1% for the week. Post-election, given the more business-friendly policies of the current administration, the market ratcheted up its growth expectations. However, with greater uncertainty caused by tariffs and federal layoffs, those growth forecasts have come down a bit leading to a rotation into defensives from cyclicals – a sign of investor caution. Defensive sectors such as healthcare and consumer staples are two of the top performing sectors year-to-date. The headline employment number for the jobs report that was released on Friday was in line with estimates, although other details in the report showed softness in the labor market. An improvement in the U.S. economic growth outlook will likely be needed before we see a positive shift in market sentiment and positioning. Decisive government policies that help reduce uncertainty could provide support as well. This week we will get more news on the inflation front with the CPI release on Wednesday.

What is going on internationally?

This year, the global focus has shifted from domestic innovation, such as AI, to international dynamics, ranging from tariffs to defense spending. This week brought several key developments:

- Germany is set to make a historic shift in its traditionally conservative fiscal policy with a proposed €500 billion Infrastructure Fund—equivalent to about 1.2% of its GDP—primarily aimed at defense and infrastructure investments. This move significantly alters its macroeconomic outlook.

- The European Central Bank (ECB) cut interest rates for the sixth time since June, bringing them down to 2.5%. However, the ECB signaled that future rate cuts will take longer, as they believe inflation is nearing their target.

- China’s Two Sessions unveiled fiscal and monetary expansion to counter weak domestic demand and external trade risks. The country remains committed to its industrial policy, emphasizing high-tech manufacturing and AI, while also addressing economic headwinds. They also targeted a GDP of 5%, lower inflation at 2%, an increased budget deficit, designed to stimulate the economy and offset sluggish consumer spending and the creation of 12 million urban jobs, highlighting a focus on employment growth and economic resilience.

These announcements highlight a broader shift in global fiscal policy, as countries ramp up spending to stimulate their economies—whether through defense investments amid reduced U.S. presence in Europe or economic support measures to counter slowing growth and rising tariffs in China.

February Jobs Report

Nonfarm employment for February rose 151k, roughly in line with consensus estimates. Most of the job gains (approximately 140k) were in the private sector. This number is close to the average monthly job gain over the past 12 months (168k). Healthcare and social assistance once again saw the strongest job gains (+63k), followed by finance (+21k) and construction (+19k). Manufacturing jobs increased 10k, most likely due to hiring ahead of the expected tariffs. Average hourly earnings increased 0.3% for the month, bringing the year-over-year rate to 4%.

Looking at other details in the report, however, shows some softness. The unemployment rate rose from 4% to 4.1%, even with labor force participation falling from 62.6% to 62.4%. Employment in the foodservice/restaurant industry fell by 28k, which could be partially due to cold weather but also may be a sign of a pullback in discretionary consumer spending. Additionally, the number of people working part-time who want full-time jobs rose 460k in February, significantly higher than the last 4 months.

Other indicators outside of the jobs report show signs of a fragile labor market as well. Job openings in December (the most recent data) fell by 556k, the largest monthly drop we’ve seen since May 2023. According to the Conference Board survey, only 33% of people think jobs are plentiful. While this number ticked up in the previous few months, it has been on a downward trend since last February, when 42.8% of people thought that jobs were plentiful. Layoffs have been stagnant though, with the layoff rate remaining at 1.1%.

Although most of the data show a continued weakening in the labor market, it’s not worrying enough for the Fed to consider cutting rates at their March meeting. Fed Chair Powell made this quite clear on Friday, as he said that “we do not need to be in a hurry, and are well-positioned to wait for greater clarity.” The market is pricing in a possible cut in June, but much of the Fed’s decision depends on inflation and the enacted policies from the administration.

Sources:

https://markets.jpmorgan.com/research/ArticleServlet?doc=GPS-4926155-0.pdf

https://markets.jpmorgan.com/research/ArticleServlet?doc=GPS-4926509-0.pdf

https://fred.stlouisfed.org/series/JTSJOL#

https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

https://yardeni.com/charts/sp-500-sectors-industries/

https://www.bls.gov/news.release/pdf/empsit.pdf