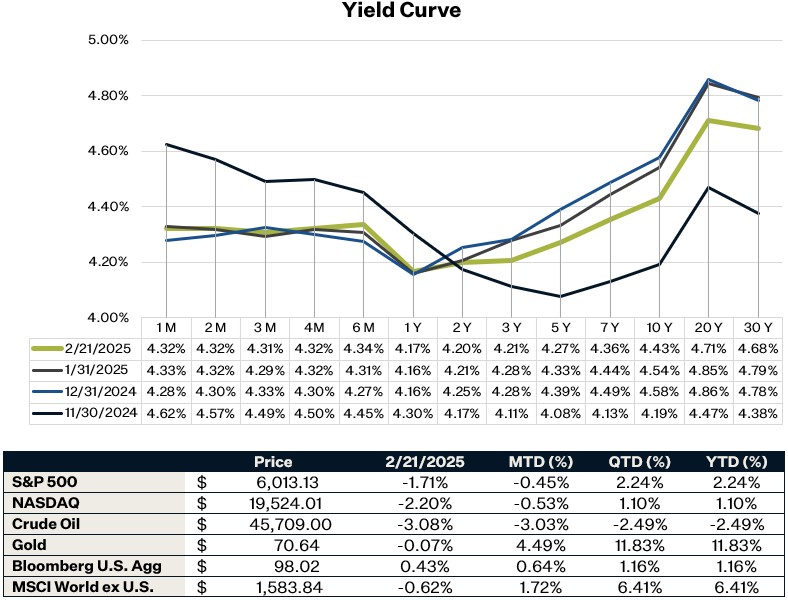

Market Update

U.S. equity markets struggled by the end of last week with Friday being the worst day of the year for equities with a reversion in the momentum factor. A weak ISM Manufacturing PMI showed U.S. business activity slowing to its weakest pace since September 2023, the S&P Global composite index fell to 50.4 (a 17-month low), and the University of Michigan survey showed that inflation expectations increased again. The services sector contracted for the first time in two years, while manufacturing growth appears temporary as firms ramp up production ahead of tariffs. Additionally, long-term inflation expectations surged to 3.5%, the highest since 1995, dragging consumer sentiment down to 64.7 amid concerns over rising costs and unemployment. As a result, stocks struggled, bond yields remained elevated, and investors reassessed the economic outlook amid growing signs of an economic slowdown. This week NVDA will report on Wednesday, which will face tough comparisons and investors will be focused on AI demand amid DeepSeek’s concerns. Additionally, on Friday the BEA will report the Personal Consumption Expenditure (PCE) Index as the market expects for it to increase 2.5% year-over-year (YoY) compared to 2.6% YoY in December.

Manufacturing and Services Sector Activity

Business activity in the U.S. grew at its slowest pace since September 2023, as the services sector contracted for the first time in two years, dragging down overall economic momentum. The S&P Global composite index fell to 50.4, the lowest level in 17 months, reflecting growing uncertainty around the Trump administration’s policies, including potential tariffs and government spending cuts. While manufacturing expanded for a second month, the boost may be short-lived, as some firms ramped up production ahead of expected trade restrictions. Meanwhile, new business inflows into services stagnated, marking the weakest growth in 10 months. Inflationary pressures also intensified, with input costs rising to a five-month high, largely due to tariffs and supplier-driven price hikes. The gap between rising costs and falling output prices is now at its widest since June 2023, threatening profit margins. Additionally, the employment gauge contracted, led by the sharpest drop in service-sector jobs since April 2020. As uncertainty looms, business optimism has faded, with expectations for future activity hitting the lowest level since September.

Q4 Earnings

Earnings for Q4 2024 continue to come in overall strong. Approximately 80% of S&P 500 companies have reported earnings, with 76% of companies beating earnings estimates. EPS growth for those that have reported is 10% year-over-year, and analysts are expecting growth to come in at 12% once the remaining companies report. Financials, Communication Services, and Consumer Discretionary lead with the highest earnings growth. Only two sectors are reporting negative growth – Energy and Materials. All eyes will be on NVDA earnings this week, which will be the final “Magnificent 7” company to report.

Michigan Consumer Sentiment

The final February University of Michigan report showed a revised consumer sentiment index of 64.7, a 3.1-point drop and below forecasts. The index's components, current economic conditions and consumer expectations also decreased. One-year inflation expectations stayed at 4.3%, but 5–10-year expectations climbed to 3.5%, the highest since April 1995. Inflation expectations have become highly partisan, with Democrats’ expectations rising sharply since the elections while Republicans’ expectations have dropped to below 1%. Independents’ expectations have risen more moderately

Sources:

Matejka, M. (2025). Equity Strategy: Q4 Earnings Season Tracker. JP Morgan.