Commodity Prices and Supply Chain Hangovers are feeding inflation and painting the Fed into a corner.

Fed Acompli: Summary

- Demand is softening: pandemic-related pent-up demand is looking like it may be easing with travel, the last of the pandemic reopening plays in full swing this summer.

- As demand wanes, oil price pressure wanes: Oil prices act as a tax on the consumer and, effectively, as parasite to the economic activity that feeds it. So, it should follow that oil prices can never stay too high for too long because they will eventually kill their host.

- Energy and food prices along with supply chain hangovers are the primary drivers of inflation, not wages: therefore, it holds that as demand softens, so too should inflation, which may help the Fed escape the need to drive the Fed Funds rate high enough to tip the fragile recovery into a recession.

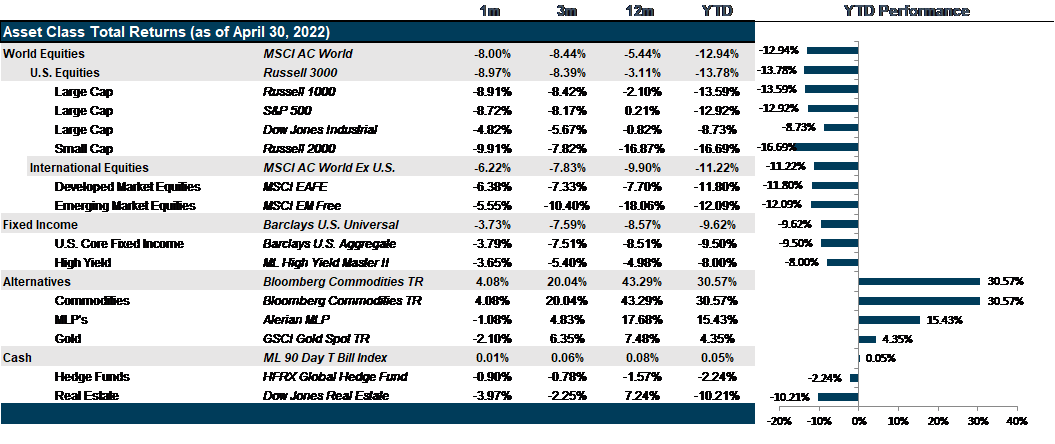

Market Review: Painful Month

Divergent central bank policies around the world, sanctions on Russia over the war in Ukraine and the lockdown in China to control fresh COVID outbreaks were the major factors impacting markets in April.

The S&P 500 lost 8.8% in April, bringing its year-to-date return to nearly -13%. The U.S labor markets have continued to remain strong with the economy adding 431,000 jobs in March and the February data being revised upwards from 678,000 to 750,000. Minutes of the March Federal Open Market Committee meeting were released in early April, with the major takeaway being the concurrence among all members on the earliest possible commencement of the process to reduce the size of the balance sheet. All options presented during the meeting involved a faster balance sheet runoff than over the 2017-2019 period. Annual inflation reportedly reached 8.5% in March, leading to markets pricing in increased possibility of a 75-bps rate hike announcement by the Federal Open Market Committee at its May meeting. In addition, big banks and major technology firms lagged expectations in their first quarterly earnings reports; large U.S banks posted steep declines in year-over-year profits, Netflix reported that it had lost 200,000 subscribers in the first quarter - falling way short of its predictions of adding 2.5 million subscribers causing the stock price to tank by 36.61%, while Amazon posted a net loss of $3.8 billion stemming largely from its stake in Rivian. The steep rise in inflation combined with a strong labor market, as well as cautious revenue guidance by companies given the U.S. GDP unexpectedly contracted by 1.4% in the first quarter of 2022, has led to increased fears of the central bank being unable to control inflation without inducing recession, which then leads to sharp contraction being observed in the U.S equity markets.

Rising food and energy costs exacerbated by the war in Ukraine has continued to affect the markets in Europe and Japan. The European Central Bank (ECB) and the Bank of Japan (BOJ) have continued to maintain an accommodative monetary stance; while the ECB has focused on reigning in their quantitative easing policy before beginning to hike rates, the BOJ has decided to double-down on expanding monetary easing by announcing daily unlimited fixed-rate bond buying operations to keep yields below 0.25% and stabilize the currency markets to prevent sharp drops in the yen compared to the dollar. The widening gap between the U.S and Japanese interest rates and the subsequent weakening of the yen is expected to benefit the export industry while easing pressure from imported inflation.

Emerging markets, primarily those in Latin America, Middle East, and Africa, have been some of the standout performers in 2022 - largely owing to soaring commodity prices driven by the war in Ukraine as well as the expulsion of Russia from emerging market indexes, which has resulted in increased weightage allocated to Brazil, South Korea, India, South Africa, and Saudi Arabia. Outlooks, however, continue to remain uncertain as various central banks continue to raise rates aggressively without much success in controlling inflation. While, China, the worlds’ top commodities importer, has imposed lockdowns to control fresh COVID outbreaks which may lead to a shrinkage in demand.

Two-year rates rose by 26 bps to 2.7% and ten-year rates rose by 50 bps to 2.89% in April, as markets priced in increased probabilities of a 50-75 bps rate hike announcement at the May meeting of the Federal Open Market Committee; along with the commencement of a speedier balance sheet runoff plan when compared to the one enacted over the period between 2017 to 2019. The sharp rise in yields has resulted in refinancing costs reaching 2009 levels and investors are moving away from long-dated securities, swapping interest-rate risk for shorter duration treasuries and credit risk as High Yield index Option-Adjusted Spreads continue to remain at historically low levels, hovering around 4%.

In commodities, WTI crude oil futures have consolidated around the $108-per-barrel price range affected mainly by the opposing forces of the proposed EU ban on Russian oil, modest supply increase announced by the OPEC+ and concerns of falling global demand stemming from COVID related lockdowns in China. Anticipation of shrinking demand from China has also pushed down prices of other industrial metals such as copper and aluminum as excess inventory when activity picks up will naturally pull-down price levels.

Going Forward: Fed Acompli

The Fed seems content to move slowly, delivering a 50 bps hike rather than the more aggressive 75 bps hike that the markets were bracing for. While that allowed for a brief respite rally, it wasn’t enough to keep the blood from flowing freely in the streets as growth stocks continued to get hammered. The higher the valuation, the more brutal the market reaction. The overall S&P 500 is starting to approach fair value, but so far, the markets are not finding a footing. Internationally, this holds true in the developed markets; however, the sell-off in emerging markets is more drawn across commodities lines than valuation lines with low value stocks that are not commodities related experiencing no mercy, suggesting a fairly dismal outlook for emerging markets generally. Meanwhile, commodities continue to perform. However, this sector is a performance vampire, sucking it’s performance out of the earnings of the rest of the economy while driving up inflation and pushing the Fed into a corner. The bloodbath in equities pales in comparison to the walloping experienced in the bond markets, whose extreme overvaluation often escaped scrutiny by investors despite nearly two decades of falling yields and expanding liquidity. One viral pandemic and one war effectively reduced the appeal of globalization, resurrected inflation, exposed unjustifiable valuations and backed the Fed into a corner. And here we are.

The View From Abroad

While the rotation back into value seems to hold true across nearly all markets, it does not hold true in emerging markets, where lines are largely drawn across commodity exposure. With the geopolitical uncertainty that now pervades the globe and the already well-known Sino-American tensions, the likelihood that these improve is largely considered by most to be nil. With the outlook for Chinese equities continuing to suffer under continued regulatory scrutiny as well as continued heavy-handed autocratic response to the continued threat of further COVID variants, the outlook for south-east Asia is also being weighed down. The only glimmer of emerging markets performance came out of Latin America, but as the outlook for commodities cools, even that small safe haven has collapsed. Meanwhile, the European Central Bank, even later to the rate hiking game than the Fed, has only stoked concern that Europe could fall into recession as it is already grappling under energy shortages brought on by Russian sanctions and severe inflation fed by the strongest dollar in almost two decades which feeds into oil prices which are priced in U.S. dollars. Japan has managed to survive the mayhem, partially on solid corporate outlooks combined with decades of undervaluation. Globally, Japan has become the safe haven for equities.

The Role of Commodities and Supply Chain

Though the resurrection of inflation has been the near singular focus, we can’t help but to recognize the roll that supply chain disruption and commodities are playing in the most recent inflation readings. More importantly is the role that wages are not playing. Though most of the inflationary basket is showing readings above their own three-year averages, it is worth noting that the largest of contributors to inflation are food, energy or supply-chain related with private transportation up 22% and public transportation up 15.3%, housing fuels and utilities up 12.2% and food at home up 9.9% on a year over year basis. Meanwhile, the components of the inflation basket most influenced by labor costs and wages are the largest laggards with medical care up 2.8%, education up 2.5%, recreation up 4.5% and apparel up 6.7% on a year over year basis. From our vantage point, this is not the kind of inflation that has momentum to it. Rather, it is almost entirely fed by commodities prices, which are currently fed by demand and supply constraints. A collapse in demand or loosening of supply constraints will almost surely be followed by a collapse in inflation. That said, demand is not collapsing yet. Far from it. Pent up demand from the pandemic has hotels, travel and tourism finally experiencing some rebound, despite higher gas prices. Though, the demand is softening for sure and gas prices are moving sideways. Moreover, inflation surprises peaked even before the year began with each new inflation reading coming in below the fantastically horrific inflation expectations that have been priced into the market. There is potential for inflation to peak and reverse in the latter half of the year based just on supply availability. However, that is not what is currently forecasted and not what the markets are priced for. Markets are priced for a hard-landing. We see some opportunity for a bounce in higher valuation, quality assets that have been repriced too severely.

The Fed

All eyes are on the Fed. Will they march forward indiscriminately towards a 2.75% Fed Funds Rate by the December meeting while the current ten-year Treasury is above 3% and the thirty-year Treasury is just a smidge above that? The result could be a yield curve that is flat as a pancake in the best of cases and severely inverted in the worst of cases. We think the likelihood of that is small as the Fed has a long history of taking a slow and steady approach. We don’t see that changing. However, until the pressure from commodities eases or wage inflation eases, we don’t see how the Fed can justify not raising rates. That said, we do see some evidence that might suggest the potential for the Fed to slow or stop the rate hikes by the fall. The first is the softening of demand and the effects that is having on oil prices, which though they are still hovering at $109 per barrel, have stopped their upward climb. Though the continued Russian sanctions are likely more to blame for the continued upward price pressure, oil prices have a self-supporting ceiling that kills demand quickly when it remains too high for too long. In fact, we see oil accomplishing an economic slowdown faster than the Fed. If so, we could see a pause in Fed tightening. However, even if we do, the tightening of financial conditions will continue as the Fed shrinks their balance sheet and the pressure on assets will favor quality assets.

Net View

We remain overweight to Growth at a Reasonable Price investments. We also remain underweight in emerging markets.