This month, we focus on the outlook for 2021 in the wake of a new political administration, a vaccine, and current market valuations. We considered several possible scenarios regarding the rollout of the vaccine, additional stimulus, and other policy changes that could shape the recovery of the U.S. economy. Our goal is not to predict outcomes, but rather to highlight the risks and opportunities of various circumstances.

Exuberance: Summary

- January was a test of sentiment: Though equities seemed to shrug off the volatility invited by the capitol riots, the slow and difficult vaccine roll out, and the digital boiler room known as the subreddit ‘WallStreetBets’, the bond markets lined up quite bearishly with the lowest volatility securities garnering the highest returns.

- Evidence of market exuberance abound: surges in SPAC’s, cryptocurrencies and IPO’s suggest too much money and too little value. Worse still, expansive fiscal policy has now given way to a small surge in breakeven inflation rates above 2%, which if accurate, would mark an end to the supportive policies sooner than Fed Funds futures are suggesting.

- Don’t forget policy: We see policy changes as potentially the biggest driver of winners and losers in the market. Given the market is clearly extrapolating the past, this could create opportunities and significant divergences in stock performance and a return to a stock-pickers market.

Market Review: Tremors in Sentiment

Markets in January were influenced by the Capitol riots, fourth quarter earnings, vaccine efficacy against mutated strains, and delays due to problems in COVID-19 vaccine supply chains.

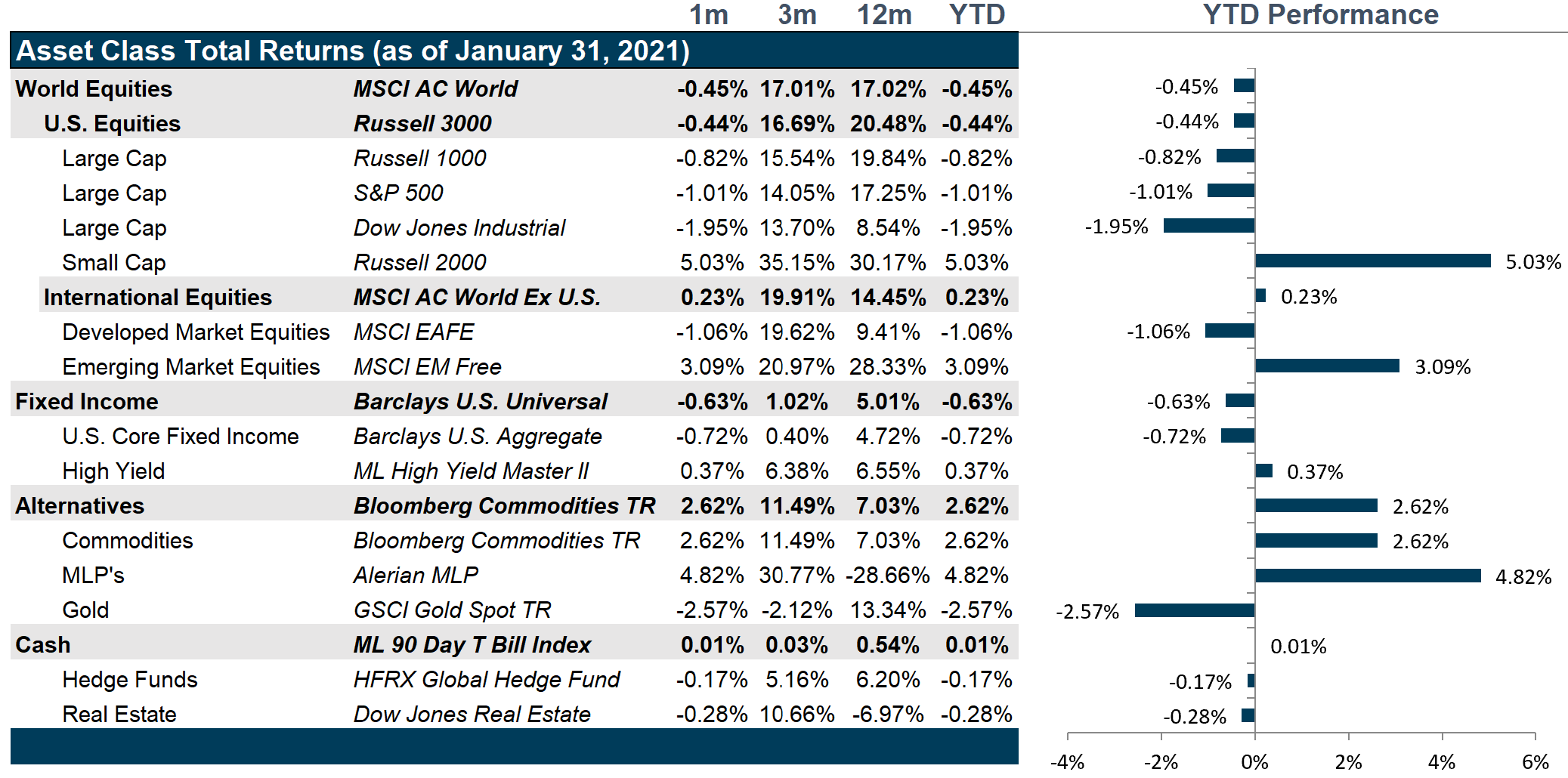

U.S. Markets

As the average price-to-earnings ratio hit historic highs, market participants began to fear that a bubble had formed. January marked a more volatile period for the markets as investors seem willing to cash in their profits at the slightest sign of uncertainty.

The month opened with markets rising in response to the second stimulus bill which was followed by the Democrats winning both Senate seats in the Georgia runoffs. This was followed by a week of selloff in Growth stocks as supporters of President Trump stormed the Capitol Building, making investors skittish.

The fall in markets remained short-lived as Joe Biden was sworn in the following week as the 46th U.S. President and his push for passing another stimulus bill worth $1.9 trillion stemmed the outflows. In addition, companies started reporting their fourth quarter earnings, and many in the Financial sector beat analysts’ estimates, resulting in the SPDR Financial Sector ETF becoming the investors’ most preferred choice for asset allocation.

Markets began to retreat from their record highs towards the last two weeks, as weekly jobless claim numbers continued to come in around 900,000, increasing inflation concerns arising from increased money supply and tightening of the labor markets.

To cap the month off, a group of retail traders, inspired by a Reddit post, attempted a short squeeze on companies like GameStop and AMC Theatres. This resulted in huge losses for the hedge funds holding the short positions and eventually huge losses for the retail traders that bought into the boiler-room-like momentum trade. This reverberated across the whole market as many investors cashed in on their profits on the back of a good earnings season and started rotating towards blue-chip stocks, precious metals, other developed and emerging markets.

International Markets

International equities witnessed a dip earlier in the month as the dollar strengthened. However, a combination of the riots in the Capitol and sudden rise in unemployment claims, led to investors diversifying their portfolios geographically while keeping their risk profile low. In addition, a strong earnings season led by Financials and Technology stocks further buoyed U.S. markets which rippled out into the international markets as well.

European markets faced uncertainty as the bloc lagged the U.S. and U.K. in vaccinating its population due to delays arising from problems in the COVID-19 vaccine supply chains.

Despite, significant inflows, the Japanese equity markets also tumbled late in the month as they faced an emergency lockdown due to rising number of coronavirus cases and deaths, which brought into question the feasibility of conducting the Olympics in August. In addition, Japan has yet to approve even a single coronavirus vaccine candidate for inoculations.

During the last week of the month, international markets fell with the U.S. markets due to the short squeeze by retail traders.

Emerging Markets

Emerging markets have had a spectacular month driven mainly by investor interest in China. China’s equity markets witnessed a record rise the past month due to an abundance of cash, low borrowing costs, and outside investors’ search for higher returns. In addition, fear of the effect of the government’s crackdown on large fintech companies took a backseat in investors’ minds as companies in China’s booming EV market, such as Tesla, Nio, Xpeng and Li Auto, reported a continued growth in bookings and sales.

The pandemic has increased the demand for electronic devices and electric vehicles which has subsequently increased the demand for semiconductors, thereby boosting the major companies listed on the stock markets of South Korea and Taiwan, with both countries leading the world in production of processors and memory chips.

Countries in the Middle East, Africa, and Europe also witnessed positive returns on account of the dollar weakening, OPEC+ gradually increasing productions and oil prices rising in response to the vaccine deployment efforts across the globe.

Interest Rates

Over the past month, the yield curved has steepened in response to the Fed Funds Rate remaining unchanged as unemployment claims have increased and inflation is rising at a much slower pace than expected. Riots at the Capitol and the short squeeze in the last week of the month further propelled long term rates and resulted in a U-shaped graph being observed in 10-year rated Treasury Bonds as well as Corporate Spreads.

Commodities

WTI Crude Oil prices rose in early January in response to the OPEC+ announcing measures to gradually ease production while keeping the group’s collective output flat as well as the decline in the strength of the dollar. The rates and demand are expected to hold steady as global vaccination efforts promise a gradual return to normalcy. Meanwhile in the near term, due to the arctic blast, the frigid winter weather hitting the U.S. Midwest and Northeast and the mid-latitude regions of Europe will drive up demand of natural gas for heating.

Gold touched a high of $1,950 per ounce due to uncertainty arising from the Capitol riots; however, it has rolled back since then and ended the month around $1,850 per ounce. Silver prices had a similar month; however, they witnessed a spike towards the end of the month as it became the next short squeeze target for Reddit retail traders. In addition, Russia announced a prolonged tax on grain exports in an attempt to curb inflation in domestic food prices, leading to wheat prices soaring globally.

Going Forward: Exuberance

We felt a tremor in equity market sentiment in January. And, then it went away.

However, the tremor in bond market sentiment did not fade as quickly. As we look across the markets, inconsistencies are becoming more and more visible. Though a recovery in earnings and eventually in the economy may do a lot to quell investor concerns and a change in administration may bring a more professional tone to policy making, the underlying fundamentals can’t be cured by money alone.

If it is not sustainable, it will not persist.

Sentiment – Stocks vs. Bonds

Measures of sentiment have continued to suggest fragility in the markets. Though the Capitol riots hardly registered, the mania egged on by the subreddit ‘WallStreetBets’ certainly woke markets up to the possibility that the normal operation of markets is not a given.

The Securities and Exchange Commission’s first directive “to protect investors, maintain fair, orderly, and efficient markets, and facilitate capital formation,” per SEC.gov, seemed to be under threat. Rampant betting in the stock markets and stock price manipulation could undermine an already fragile market. However, the government’s ability to get ahead of this new digital age with regulation has so far been found wanting with technology changing the game before law makers can figure it out, much less establish efficient rule making.

The underlying efficient operation of markets could be perhaps the largest existential threat to markets that is not priced in. However, equity markets have quickly shrugged it off breaking a value streak that had finally established itself.

Growth and technology have surged as of late as earnings cheered the markets back up. Though the vaccine roll out has been poor and pandemic caseloads continue to surge, investors still believe the recovery is here and the economy will reopen by summer.

Bond markets, on the other hand, lined up rather bearishly with the lowest volatility instruments garnering the highest returns for January.

One of these markets will turn out to be wrong.

Exuberance – Asset Inflation vs. Real Inflation

Excess money growth has historically stoked fears of inflation. Debt creation, whether at the government level through fiscal stimulus or at the corporate and household levels through monetary stimulus, creates excess demand.

When demand is low, countercyclical stimulus should have few inflationary effects. However, keeping stimulus on too long can, in theory, produce excess demand and price increases that can disrupt economic growth.

That said, it has been so long since we have seen measurable inflation in the U.S. economy, that many are beginning to wonder if we are, perhaps, measuring the wrong things. Or worse, if the connection between monetary stimulus and demand is possibly not as strong as it used to be.

We see this as a little bit of both. While the price of goods and services seems to remain somewhat steady, money growth seems instead to be channeled into savings and investments, fueling asset price inflation rather than traditional inflation, which can be equally disruptive and highly unequal in its distributional effects.

We note the excess price movements of riskier and riskier market instruments as evidence of asset price inflation, or perhaps even bubbles. Meanwhile, excess money is not making its way into wage inflation spurred by policy-induced increases in spending and money velocity. That persistently low money velocity keeps a cap on traditional inflation, and it also suggests that inflation, as measured by the Federal Reserve Bank and which informs monetary policy decisions, is a very long way off.

Yet, breakeven inflation is trending above 2% while Fed Funds futures are projecting near zero rates until 2022.

One of those will be wrong.

Policy – The Government vs. The Markets

Key policies coming out of the Biden Administration have the potential to profoundly change the outlook for sectors by either raising the cost of doing business or by wiping out business models altogether.

A study of European policies over the past several years could offer a hint. Issues of environmental regulation, labor policy, and interactive media platform liability are the first and most obvious policies to offer game changing outlooks.

We see disruption across the already beaten down energy sector with the aggressive shift toward clean energy. We also see impacts to consumer discretionary margins with the shifts in labor policy. However, the most aggressive valuations in interactive media and services on issues such as privacy, liability protections afforded by Section 230 of the Communications Decency Act, and anti-trust lawsuits against Google, Amazon, and Facebook could reshape the way these companies can continue to evolve.

With so much extrapolation of earnings and margin trends priced in at such a fragile and debt-laden moment in the broad markets, investors should be considering policy and regulation scenarios along with economic demand scenarios when considering portfolios.

“The only thing that is constant in life is change.” – Heraclitus

Net View

We are shifting to a neutral stance in growth versus value and instead focus on capitalization.

Within equity, we are recommending an overweight to small capitalization stocks relative to large capitalization stocks.