We continue to focus on the challenges of growing into current valuations in the face of rising inflation and the removal of monetary stimulus.

The Beginning of an End: Summary

- An economic recovery is underway in the U.S. with some challenges: a resurgence of COVID, and a great resignation and supply chain challenges cannot seem to stop U.S. determination to stage an economic recovery and may make the recovery more robust as a result.

- Lingering inflation resulting from rising wages along with increased manufacturing and logistical costs have pushed the Fed to contemplate a speedier removal of liquidity: the resulting pressures on valuation and earnings quality will continue to support value and growth-at-a-reasonable-price (GARP) investments, and could be very negative for fixed income investments.

- If the Omicron variant does mark the beginning of the end, then international equities may start to look attractive once again: European and Japanese equities remain significantly undervalued relative to U.S. equities while experiencing nearly three times the earnings growth during the recovery.

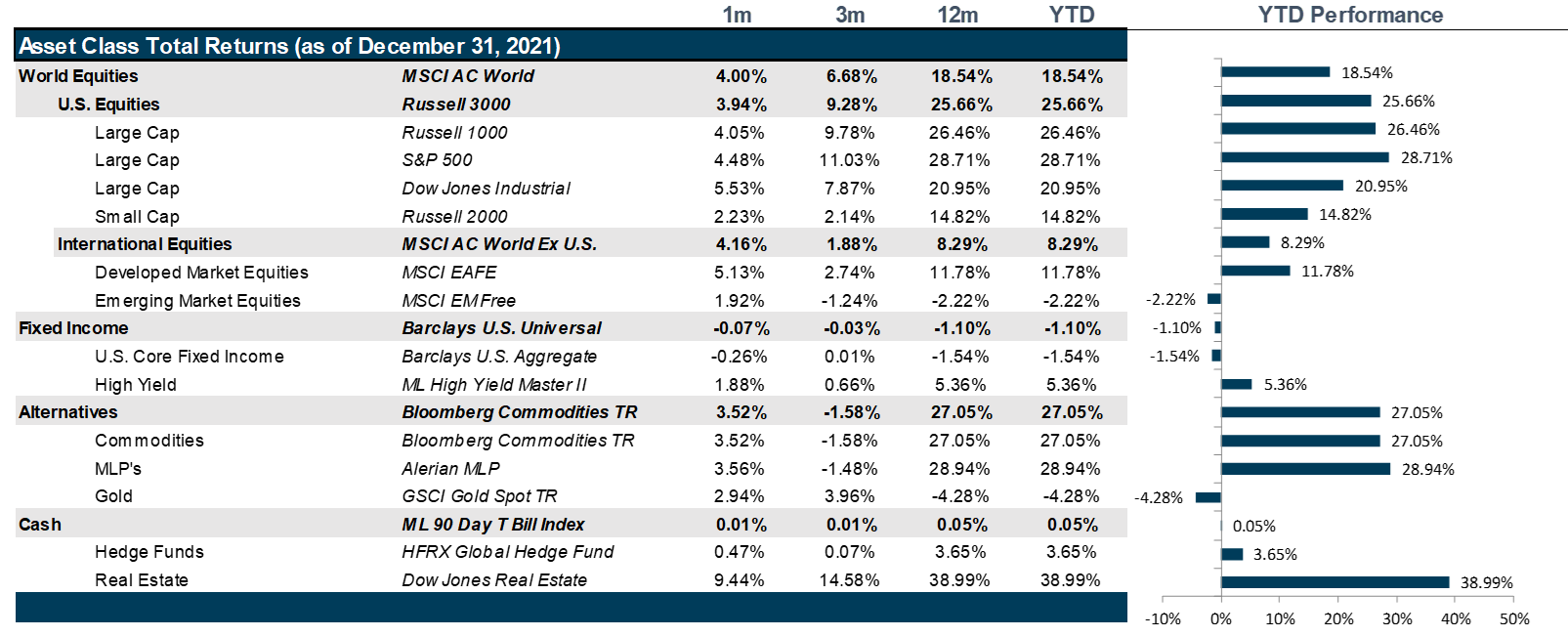

Market Review: Bad But Not Terrible

December, markets reacted to the spread and effects of the new Covid-19 variant Omicron, a more hawkish Federal Reserve, and the imminent failure of President Biden’s Build Back Better bill.

U.S. equity markets endured bouts of volatility in December. The discovery of the Omicron variant in South Africa and subsequently in Europe fueled selloffs in the last week of November, only to see market reverse in the first weeks of December as anecdotal evidence of those infected with the new variant revealed much milder symptoms compared to the Delta variant. Emergency approvals granted to Pfizer’s antiviral COVID-19 pill by the Food & Drug Administration further alleviated COVID-related worries. However, continued supply chain disruption continued to loom over holiday shopping, feeding already aggravated inflationary fears. The Federal Reserve began adopting a more hawkish picture announcing faster rate hikes and withdrawal of monthly bond purchases to combat inflation. Weekly jobless claims numbers have solidified around the 200,000 range while the jobs report for November was disappointing adding only 210,000 jobs, half of what economists were expecting. Inflation continued to rise with the Consumer Price Index increasing by 0.8% in November. Yet, while the labor data was disappointing, the jobs market continued to increase the number of positions being filled and unemployment claims continued to fall consistent with the recovery in progress, allowing the Federal Reserve to shift gears and combat inflation with a greater degree of urgency.

As the holidays drew near, West Virginia Senator Joe Manchin threw markets into a tail-spin by refusing to vote in favor of President Biden’s Build Back Better bill in the evenly split Senate, effectively dooming it. Markets recovered towards the last week of the month, though low trading volumes reduced the reliability of any inferences drawn from it. Overall, REITs continued to be the top performer with the S&P 500 REIT Index gaining 8.57% over the past month and 43.05% over the year. Supply chain issues have led to companies leasing more warehouses to store additional inventory as well as bringing back certain segments of manufacturing to the U.S.. Steadier cash flows and long-term triple net leases also make this sector appear relatively recession proof, establishing it as a favorite of investors.

The discovery of the Omicron variant in Europe led to a major selloff in early December followed by an uncertain recovery and another selling spree following U.S. markets ahead of the holidays. While European markets rose slightly during the holiday-thinned trading, rising energy costs and central banks shifting away from easy policy to combat inflation might lead to reduced returns in 2022. Japanese markets were affected by the impact of the Omicron variant on their U.S. and European counterparts, however a recovery took hold in the latter half of the month as the index gauging big manufacturer’s sentiment remain unchanged from the previous quarter, while tracking big non-manufacturer’s sentiment improved for the sixth straight quarter.

Emerging markets continued to lag their counterparts down in December. While the Omicron variant led to a global selloff, the subsequent recovery seems largely muted among emerging market indexes. China’s stringent Covid policies are affecting its economic recovery while the housing market continues to stumble. Foreign investors have remained concerned as Chinese stocks face delisting risks and increased government crackdown along with an increasingly frosty relationship between China and the U.S. that has made it less conducive to invest.

The yield curve steepened considerably in December as the Federal Reserve adopted a hawkish stance towards combating inflation by looking to further reduce the monthly bond purchases while accelerating the timeline of rate hikes, with two to three hikes expected in 2022.

Energy prices fell in mid-December owing to rising Omicron cases worldwide as well as the rejection of President Joe Biden’s Build back better bill by Democratic Senator Joe Manchin. However, the energy complex staged a recovery over the holidays as Omicron proved to be less severe with WTI Crude Oil closing the year at $76 per barrel. The deep energy crunch in Europe also points towards a difficult transition from non-renewable to renewable sources of energy. In addition, a mismatch between demand and supply pushed Chicago lumber futures to above $1100 per thousand feet as housing construction continued to rise, while labor shortages and weather disruptions affected logistics.

Going Forward: The Beginning of an End

As the new year begins, the world seemingly remains trapped in a repeating pattern of pandemic surges. However, the latest edition features a run-away virus with significantly fewer hospitalizations and deaths occurring with an economic recovery in the backdrop. The resulting clash between the two phenomena seems to exacerbate last year’s story which focused on wealthier countries getting vaccinated and reopening while poor countries remained locked down and unable to fulfill their roles in the global supply chain. The surge in inflation started with a build of massive economic stimulus that created a surge of pent-up demand that was unleashed with each attempt at economic reopening. Initially, inflation was fed by the stumbling of the global supply chain and then further stoked by the great resignation as members of the labor market demanded better pay, safer working conditions and greater work flexibility. The combination has delivered a one-two punch to an economy that has largely gotten used to high margins and non-existent inflation in the traditional sense. The resurgence of inflation has heralded hawkishness in the Fed right at the same time that the fiscal party my be coming to an end. As the liquidity tide ebbs this year, we will learn who is swimming naked, to harken back to Warren Buffet’s famous quote, “Only when the tide goes out do you discover who’s been swimming naked.” The rush for quality could be epic this year.

Continued Recovery

Despite a slowdown in economic expectations and a pick-up in inflation expectations, the data is still, on the whole, constructive globally with parts of Southeast Asia finally starting to emerge from the pandemic. Though earnings have been on fire all year, next year is expected to continue to deliver strong numbers, despite higher costs. Parts of the market are experiencing margin expansion despite high costs because strong demand has allowed companies with pricing power to reset prices, which further feeds inflation, but in a positive way. So, growth is not going away anytime soon, but exuberance may start to fade, which could put pressure on low quality companies and unjustifiably high valued companies alike.

Evaporating Liquidity

Further putting pressure on valuations is the realization at the Fed that they may have to act faster than planned to combat the lingering inflation. First, the Fed is aggressively planning to dial back it’s bond buying program, thus stopping the expansion of it’s balance sheet. It will follow this with an expected run-off period during which the Fed will allow it’s balance sheet to shrink further by letting bonds mature without replacing them. At the same time, the Fed is expected to start hiking rates as soon as March. Three rate hikes are currently priced into the Fed Funds futures markets, bringing the Fed Funds rate to 75 bps by the end of 2022. And, this may seem challenging, keep in mind that treasury yields surpassed S&P 500 dividend yields in 2021 and the spread remains negative. Unless equity prices move, this will only get worse in 2022. Couple this with the notion that further fiscal expansion is growing less and less likely, meaning that 2022 will have no stimulative support and will have to depend on real growth to support valuations. This is where the quality argument gets stronger. As markets reset, we can expect a rush to quality across asset classes.

Looking Abroad

As the argument for seeking out quality earnings should favor U.S. equities, valuations do not. Europe is cheap, Japan is cheaper and Emerging Markets are in the bargain basement. And, if Omicron does indeed turn out to outcompete Delta for susceptible victims without killing them and leaving a path of immunity in its wake, then the markets that are farthest behind have the most to catch up. In fact, looking across markets, while U.S. markets have turning in solid earnings growth, they remain highly overvalued compared to their global counterparts who have delivered multiples of earnings growth and remain very undervalued. Over the last twelve months, the S&P delivered a whopping 48% earnings growth and 2% dividend yields and currently trades at 25x earnings. Meanwhile, European companies delivered 175% earnings growth a 4% dividend yield and are trading at a paltry 17x earning, as an example. Parts of Emerging Markets, such as Mexico, are equally appealing having turned in 144% earnings growth and currently trading at 15x earnings. Though, we are not constructive on China and do not necessarily believe that EM will outperform developed international markets, we could envision European and Japanese equities staging a battle against U.S. equities as the dollar will likely strengthen as interest rates rise, further boosting sales abroad and dampening U.S. multinational sales. Dollar strength, however, will act as an equalizing force for U.S. dollar-based investors, who will have to overcome losses due to currency exchange.

Net View

We remain neutral in growth relative to value, though resume our overweight to GARP. We also remain underweight in Emerging Markets relative to the U.S., but overweight Latin America within Emerging Markets moving toward an overweight in Europe relative to international equities.